The Sunk Cost Fallacy — Meaning, Examples & How to Overcome It

Mind · Cognitive Biases · Decision & Action family

Test yourself — can you spot the bias in each scenario? Take the Cognitive Bias Spotter Test. Jump to the test ↓

What Is the Sunk Cost Fallacy? Simple Definition

The sunk cost fallacy is the tendency to continue investing time, money, or effort into something because of what you have already put in — rather than because of what it is likely to return in the future.

In simple terms: past investment should have no bearing on whether you continue something. The money is gone whether you stop or carry on. The hours are spent whether you finish or quit. Rational decision-making looks only at future costs and future benefits. The sunk cost fallacy is what happens when past losses hold future decisions hostage.

This page is part of the cognitive biases guide on our brain training and cognitive testing platform, alongside interactive tests and tools covering memory, attention, and decision-making.

Sunk Cost Fallacy Meaning & Psychology

You have spent three hours at a concert you are not enjoying. You could leave — but you paid £80 for the ticket, and leaving feels like wasting that money. So you stay, adding three more hours of discomfort to a loss that is already complete. Or: a company has invested £50 million in a product development project. Six months from launch, internal testing reveals the product will likely fail in the market. The rational decision is to cut losses. Instead, the board authorises another £20 million — because stopping now would mean "wasting" the £50 million already spent. The £50 million is gone either way. It is not on the table.

The sunk cost fallacy has been studied extensively in behavioural economics. The foundational framework comes from Arkes and Blumer (1985), who demonstrated in a series of experiments that people systematically allow prior expenditure to influence future decisions even when that expenditure is objectively irrelevant. In one of their most cited studies, people who had paid more for a ski season ticket used it more frequently than those who had paid less — not because they enjoyed skiing more, but because the higher prior expenditure created stronger pressure to justify the investment.

Why the brain does this

The sunk cost fallacy is driven by loss aversion — the well-documented asymmetry in how humans experience losses and gains identified by Kahneman and Tversky (1979) in their work on prospect theory. Stopping a failing project does not just mean accepting a future without that project's returns — it means converting an uncertain loss into a confirmed one. The mind treats the unrecoverable investment as still potentially retrievable if you just persist long enough, because stopping makes the loss final and undeniable. Continuing keeps alive the possibility, however slim, of eventual justification.

The role of identity and commitment

Sunk costs are particularly powerful when the investment is tied to identity or public commitment. A founder who has spent five years building a company is not just weighing financial returns — they are weighing what stopping says about them, about their judgment, about the years of their life they devoted to the venture. Admitting the project should end feels like admitting those years were wasted, which triggers not just financial loss aversion but ego threat. This is why sunk cost reasoning is especially entrenched in founders, long-tenured employees, and anyone who has publicly championed a course of action.

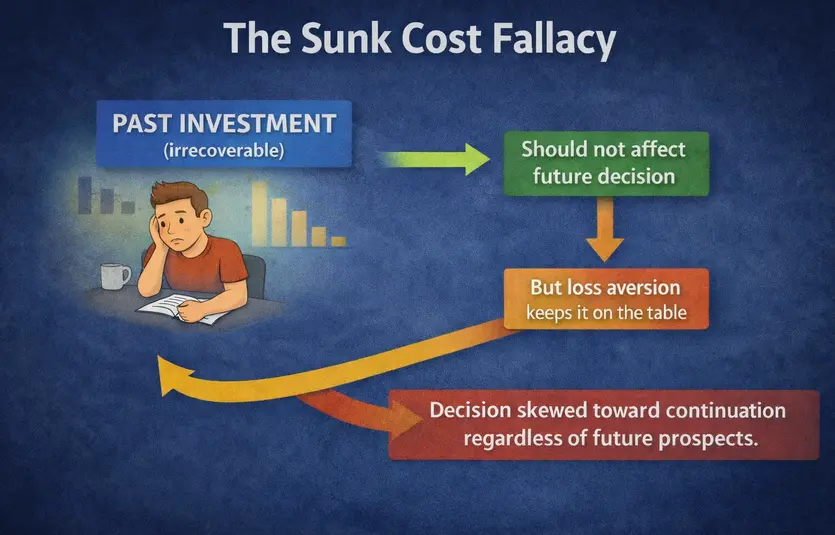

The sunk cost fallacy — past investment should have no bearing on future decisions, but loss aversion keeps it on the table and skews the decision toward continuation regardless of future prospects.

Sunk Cost Fallacy in Real Life — Examples

The sunk cost fallacy appears wherever people have invested something they cannot get back. Finishing a meal you no longer want because you paid for it. Watching a film to the end even though it is clearly bad — because you are already an hour in. Staying at a party you are not enjoying because you made the effort to get there. In each case the investment is complete and irrecoverable; the only question is whether continuing adds value going forward. In each case, the past investment is answering that question instead.

The effect is particularly strong when the sunk cost is large, recent, or visible. A small expenditure produces a mild sunk cost pull; a large one can dominate decision-making entirely. This is why the fallacy tends to show up most consequentially in exactly the situations where the stakes are highest — major financial investments, long-term projects, significant personal commitments — precisely the decisions where rational forward-looking analysis matters most.

Sunk Cost Fallacy in Investing and Finance

In investing, the sunk cost fallacy manifests most clearly as the reluctance to sell a losing position. An investor who bought a stock at £100 and watches it fall to £60 faces a psychologically asymmetric choice: selling at £60 converts a paper loss into a real one, making it final and undeniable. Holding on keeps alive the hope of recovery. The rational question — would I buy this stock today at £60 given what I know? — is almost never the question investors are actually asking. They are asking: how do I avoid confirming that I lost £40?

This connects closely to the disposition effect — the documented tendency of investors to sell winning positions too early and hold losing ones too long — which is driven substantially by sunk cost reasoning combined with loss aversion. The result is portfolios that are systematically overweighted in poor performers and underweighted in strong ones, precisely because the past purchase price anchors the decision to hold or sell in a way that has no rational basis in forward-looking analysis. This also overlaps with anchoring bias — the original purchase price functions as an anchor against which current value is measured, making a recovery to that price feel like the minimum acceptable outcome.

Sunk Cost Fallacy in Relationships

The sunk cost fallacy is one of the most psychologically powerful drivers of staying in relationships that are no longer working. Years of shared history, emotional investment, and the identity built around the relationship all function as sunk costs that make the prospect of ending things feel like confirming those years were wasted. The question that sunk cost reasoning asks is: given how much I have put into this, how can I walk away? The question forward-looking analysis asks is: given what this relationship is and what it is likely to become, does continuing it serve my interests and the other person's?

The sunk cost pull in relationships is amplified by social visibility — the awareness that others have witnessed the investment, attended the wedding, met the partner — which adds a layer of public justification to the private psychological pressure. Leaving requires not just accepting a personal loss but explaining it to a social network that has been watching the investment accumulate.

Sunk Cost Fallacy in Business and Management

In organisational settings, the sunk cost fallacy produces what is sometimes called escalation of commitment — the tendency to increase investment in a failing course of action precisely because of the investment already made. The classic business case is the development project that has overrun its budget, missed its deadlines, and produced evidence that its fundamental premise was flawed — but which continues to receive funding because the accumulated investment makes stopping feel catastrophic.

Research by Staw and Ross (1989) established that escalation of commitment is a pervasive feature of organisational decision-making, and that it is particularly pronounced when the same person or team who made the original investment decision is responsible for evaluating whether to continue. Personal accountability for the original decision creates ego investment that compounds the financial sunk cost, making objective reassessment structurally difficult. This is one of the strongest arguments for separating the people who initiate projects from those who periodically evaluate whether they should continue.

Sunk Cost Fallacy in Education and Career

Career and educational sunk costs are among the most consequential and least discussed. A person who has completed two years of a degree they no longer want faces a powerful sunk cost pull to finish — the two years already spent feel like they will be wasted if the degree is not completed. But the two years are spent regardless. The forward-looking question is: given the remaining cost in time and money, and the likely return from this specific qualification, is completing this degree the best use of those resources? Sunk cost reasoning makes this question almost impossible to ask, let alone answer honestly.

The same pattern applies to careers: a professional who has spent fifteen years building expertise in a declining field faces enormous sunk cost pressure to stay, because leaving means the fifteen years feel wasted. The rational question — where is my skill set most valuable going forward? — is buried under the weight of past investment. The result is often that people remain in careers or roles well past the point where changing direction would serve them significantly better.

How to Avoid and Overcome the Sunk Cost Fallacy

Ask the "fresh start" question

The single most effective reframe is to ask: if I were starting from zero today — no prior investment, no prior commitment, no history — would I choose to begin this project, relationship, or course of action given what I now know? If the honest answer is no, then the sunk cost fallacy is likely what is keeping you in. The past investment is the only argument for continuing; the forward-looking analysis says stop. Separating those two questions clearly is the core skill.

Separate the decision from the person who made it

In organisational settings, one of the most reliable structural countermeasures is to ensure that the people evaluating whether a project should continue are not the same people who initiated it. External review, stage-gate processes with independent assessment, and pre-defined exit criteria all reduce the personal ego investment that compounds sunk cost reasoning. When the person reviewing the decision has no stake in the original one, forward-looking analysis becomes substantially easier.

Reframe what "waste" means

The psychological power of sunk costs comes from the feeling that stopping wastes past investment. Reframing helps: the investment is already spent — what is actually at risk of being wasted is the future resources you will put in if you continue without good reason. Continuing a bad investment does not recover the past; it adds future loss to completed loss. What is waste is not stopping — what is waste is the additional time, money, and opportunity cost of continuing past the point where the evidence says stop.

Set exit criteria in advance

Before beginning any significant investment — a project, a financial position, a commitment — define in advance the conditions under which you would exit. What performance level, after what time period, would lead you to stop? Writing these criteria down before the investment begins, when sunk cost reasoning has not yet taken hold, creates a pre-committed standard against which future continuation can be objectively measured. This is the same principle behind stop-loss orders in investing: the exit decision is made when judgment is clear, not when loss aversion is at its peak.

The Deeper Point

The sunk cost fallacy is not a failure of intelligence — it is a failure of the framing through which decisions are evaluated. The past investment is real, the emotional weight of it is real, and the social pressure to justify it is real. What is not real is its relevance to the forward-looking question of whether continuing serves your interests. Keeping those two questions separate — what has been spent, and what should be done next — is harder than it sounds precisely because the mind treats them as one.

Understanding the sunk cost fallacy changes how you evaluate persistence. Persistence is a virtue when the forward-looking case for continuing is strong; it is a trap when the only argument for continuing is the investment already made. Learning to tell the difference is one of the most practically valuable things an understanding of cognitive bias can produce.

Related biases that interact closely with this one: anchoring bias, where the original investment price anchors all subsequent evaluation; confirmation bias, which ensures that evidence supporting continuation is noticed and evidence supporting exit is minimised; and loss aversion, the underlying mechanism that gives sunk costs their psychological power.

The Cognitive Bias Spotter Test below puts that understanding to work — see if you can catch the sunk cost fallacy and the other nine biases when they appear in realistic scenarios.