Endowment Effect — Meaning, Examples & How to Overcome It

Mind · Cognitive Biases · Judgment & Decision-Making family

Test yourself — can you spot the bias in each scenario? Take the Cognitive Bias Spotter Test. Jump to the test ↓

What Is the Endowment Effect? Simple Definition

The endowment effect is the tendency to value something more highly simply because you own it. The same object — a coffee mug, a house, a share in a company — is worth more to the person who already has it than to someone who does not, even when there is no rational basis for this difference in valuation. The act of ownership inflates perceived value. What you would demand to give something up is systematically higher than what you would pay to acquire the same thing — a gap that standard economic theory predicts should not exist, but that appears reliably across a wide range of goods, contexts, and populations.

This page is part of the cognitive biases guide on our free brain training and cognitive assessment platform, alongside interactive tools covering memory, attention, reaction time, and decision-making.

Endowment Effect Meaning & Psychology

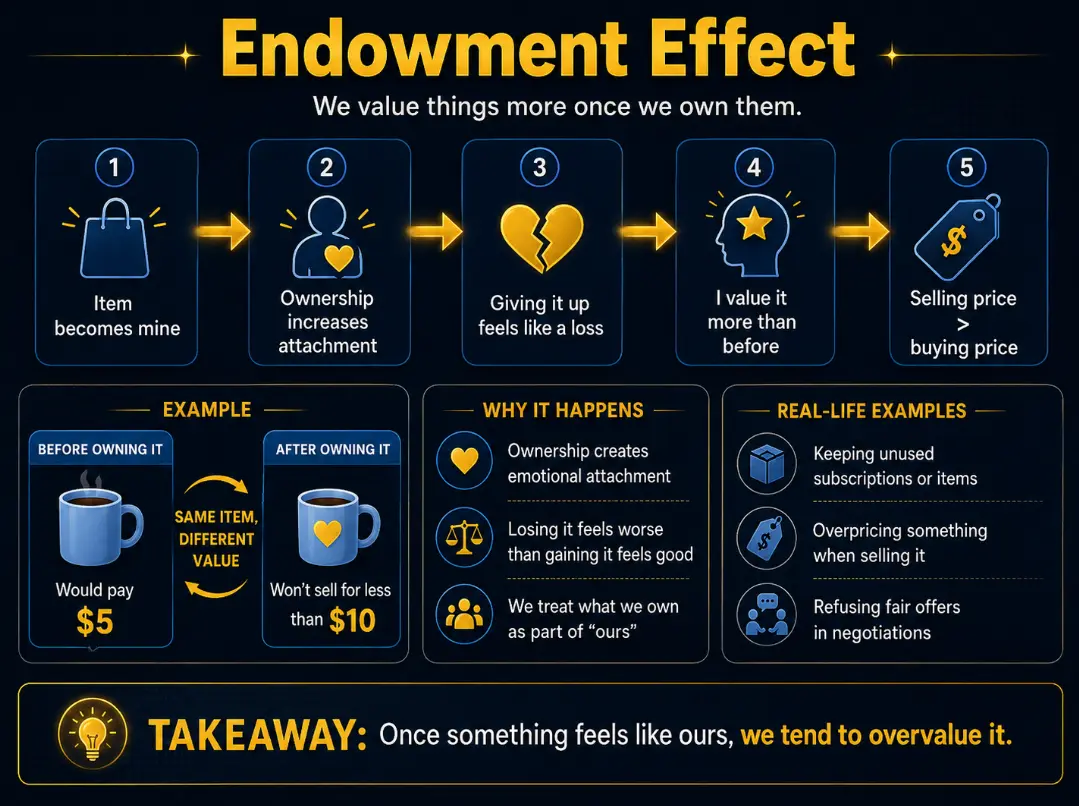

The endowment effect was named by Richard Thaler in 1980, who identified it as a manifestation of loss aversion — the asymmetry in prospect theory whereby losses loom larger than gains of equivalent magnitude. Giving up something you own is psychologically coded as a loss; acquiring something you do not own is coded as a gain. Because losses are felt more acutely than equivalent gains, the minimum price you will accept to sell something (willingness to accept, or WTA) exceeds the maximum price you will pay to acquire the same thing (willingness to pay, or WTP). Ownership converts a neutral transaction into a potential loss, and loss aversion inflates the price required to accept it.

The foundational experimental demonstration came from Kahneman, Knetsch & Thaler (1990), who conducted a series of market experiments using everyday objects — most famously coffee mugs. Half the participants were randomly given a mug; the other half were not. All participants were then asked either the minimum price they would accept to sell their mug, or the maximum price they would pay to buy one. The Coase theorem from economics predicts that because mugs were randomly assigned, roughly half should trade — those who received mugs but value them less than the market price should sell to those who value them more. In practice, observed trading volume was consistently far below the predicted level, and median selling prices were approximately twice median buying prices. Ownership alone — randomly assigned — had doubled the perceived value of the mug.

A broader review by Kahneman, Knetsch & Thaler (1991) placed the endowment effect within a wider family of loss-aversion anomalies, connecting it to status quo bias and the general principle that departures from the current reference point are evaluated asymmetrically — losses hurt more than equivalent gains feel good, producing a systematic bias toward retention of what is already possessed.

Psychological ownership and the endowment effect

Subsequent research has shown that the endowment effect does not require legal ownership — it can be triggered by psychological ownership, the sense of having a connection to or control over an object even before formal acquisition. The effect begins to develop within seconds of being given an object, and can be induced by simply asking people to imagine owning something. This has significant practical implications: retailers and car dealerships that allow customers to handle products, take test drives, and customise options are exploiting the endowment effect by creating psychological ownership before any purchase is made.

The endowment effect: once something feels like ours, we overvalue it. The same coffee mug a person would buy for $5 they will not sell for less than $10 — ownership converts the transaction into a potential loss, and loss aversion inflates the price.

Endowment Effect in Real Life — Examples

In property markets, the endowment effect is one of the most consequential influences on pricing behaviour. Homeowners consistently set asking prices that reflect their own inflated valuation of their property — the result of years of ownership, personal attachment, and the coding of a sale as a loss rather than an exchange. This produces a systematic gap between sellers' expectations and buyers' valuations that prolongs time on the market, reduces transaction volumes, and contributes to the well-documented tendency of homeowners to hold out for prices that the market will not sustain. Studies of housing markets following price declines have shown that owners with negative equity — who face the prospect of a nominal loss on their purchase price — hold out for significantly longer and trade at lower volumes than those who can sell at a gain, a direct endowment effect combined with loss aversion.

In financial markets, the endowment effect contributes to the disposition effect — the tendency for investors to hold losing positions too long and sell winning positions too soon. Once a stock is held, selling it at a loss is coded as realising a loss, and loss aversion makes this more painful than the rational valuation of the position warrants. The stock is worth more to its current owner than to the market, and the gap between their minimum selling price and the market price produces inertia that persists even as the fundamental outlook deteriorates.

In negotiation, the endowment effect produces asymmetric valuations that complicate exchange. The seller's minimum acceptable price and the buyer's maximum acceptable price are both influenced by ownership — the seller's by the inflated value of what they are giving up, the buyer's by the more moderate value of what they would be gaining. This gap reduces the zone of possible agreement and increases the frequency of failed negotiations that would have been mutually beneficial if both parties had evaluated the object at its market value rather than through the lens of loss aversion.

Endowment Effect in Consumer Behaviour

Free trials, money-back guarantees, and easy return policies all exploit the endowment effect. Once a consumer has possession of a product — even on a trial basis — psychological ownership begins to develop, and the prospect of returning it is coded as a loss. Return rates for trial products are typically far lower than the rate at which consumers would have voluntarily purchased the same products, because the endowment effect raises the effective price of giving them back. Retailers who offer generous return policies benefit from this: the policy reduces the perceived risk of purchase, which increases purchase rates, while the endowment effect reduces actual returns.

Personalisation and customisation similarly strengthen the endowment effect. A product that has been configured, named, or modified to reflect the consumer's preferences feels more owned — more part of the self — than a standard off-the-shelf version, and is correspondingly harder to give up or return. This is why car configurators, monogramming services, and subscription personalisation flows are ubiquitous in consumer product design: they are endowment effect amplifiers.

Endowment Effect vs. Mere Ownership Effect

The endowment effect is sometimes distinguished from what researchers call the mere ownership effect — the tendency to evaluate objects more positively simply because one owns them, independent of any prospective transaction. The mere ownership effect operates in evaluation and attitude; the endowment effect operates most clearly in exchange and pricing. Both reflect the same underlying mechanism — ownership changes the psychological relationship to an object — but the endowment effect's clearest signature is the WTA-WTP gap: the divergence between what people demand to sell and what they would pay to buy the identical thing. This gap is the hallmark of loss aversion operating through the reference point of current ownership, and it connects directly to status quo bias — the broader tendency to prefer what one already has over alternatives, driven by the same asymmetric coding of departures from the current state.

How to Overcome the Endowment Effect

Ask what you would pay to acquire it, not what you would accept to sell it

The most direct counter to the endowment effect in pricing and valuation decisions is to shift the frame from seller to buyer. Rather than asking "what would I accept for this?", ask "if I did not already own this, what would I pay for it?" The buyer-frame activates a different reference point and typically produces a more accurate market valuation. If the answer to the buyer-frame question is substantially lower than the answer to the seller-frame question, the gap is the endowment effect — and the buyer-frame answer is the more reliable estimate of the object's actual market value.

Separate the object from its ownership history

The endowment effect is amplified by personal associations — memories, experiences, and identity connections that accumulate around owned objects over time. Deliberately evaluating an object on its functional and market merits, separate from its ownership history, reduces the contribution of these associations to perceived value. In property decisions, this means assessing the house as a buyer would assess it rather than through the lens of the life lived in it. In financial decisions, it means evaluating a position on its current prospects rather than on what was paid for it — a corrective that also addresses the sunk cost fallacy, which similarly inflates the value of past investment.

Recognise the loss aversion component explicitly

Because the endowment effect is driven by loss aversion, naming the mechanism — "I am asking for more than this is worth because giving it up feels like a loss" — can reduce its influence. Research on debiasing suggests that understanding the mechanism of a bias does not eliminate it, but it creates a cognitive wedge between the automatic response and the final decision. Recognising that the pain of giving something up is not a reliable signal of its value is the first step toward adjusting valuations toward a more accurate baseline. This connects to the corrective for framing effect — restating the transaction in gain terms rather than loss terms can reduce the asymmetric aversion that inflates the seller's price.

The Deeper Point

The endowment effect reveals that value is not an intrinsic property of objects — it is a relationship between an object and its owner, shaped by the psychological fact of possession. What something is worth to you depends substantially on whether you already have it, because having it converts any transaction into a prospective loss, and loss aversion inflates the price of loss beyond what the object's intrinsic utility warrants.

This has consequences across markets, negotiations, and personal decisions wherever the party who owns something and the party who might acquire it need to agree on a price. The endowment effect systematically widens the gap between their valuations, reduces the volume of mutually beneficial trades, and produces holding patterns — in property, in finance, in personal possessions — that are maintained long past the point where rational valuation would support them.

Related biases worth exploring alongside this one: status quo bias, which is the broader preference for the current state driven by the same loss aversion mechanism; sunk cost fallacy, which similarly inflates the value of past investment in the decision to continue; and framing effect, whose loss-frame power is the underlying mechanism that makes ownership so consequential to perceived value.

The Cognitive Bias Spotter Test below puts that understanding to work — see if you can identify the endowment effect and the other nine biases when they appear in realistic scenarios.